Diving in with Donor Acquisition Cost

Part 3 of 6 in Our Data-Driven Fundraiser’s Reference Guide

On this page

Getting started

Donor acquisition what?

What is donor acquisition cost

How to calculate donor acquisition cost

Why measure donor acquisition cost

Donor acquisition cost best practices

Key takeaways

Getting started

Donor acquisition cost is far from trivial, and that is why for part three of our six-part series, Data-Driven Fundraiser’s Reference Guide, we will take a deeper look into the importance of questioning, testing and measuring this key fundraising metric.

This is the first piece in this series that takes a deep dive into a specific metric. The first two parts of Data-Driven Fundraiser’s Reference Guide have been more high-level and introductory. This section, especially when paired with the soon-to-be released part four, will be geared towards application and best practices.

Let’s get started!

Get Data-Driven Fundraiser Email Updates

Donor acquisition what?

“How much did this donor cost?”

There was an awkward silence on the other end of the line.

“I’m not sure, maybe $50, maybe $100.” I was speaking with the Director of Development at a small nonprofit in Minnesota. “I think that donor came from our year-end appeal,” the confounded fundraiser carried on.

One of our client’s donations were growing year over year, and they wanted to figure out how to continue the trend. We helped them analyze their donor database and found that they were doing a good job of acquiring new donors, but a lot of donors were lapsing. We focused on developing a retention strategy to keep donors around after their first gift.

Taking in to account donor acquisition cost, we realized for our client (like most organizations) it’s much less costly to retain donors after their first gift than to acquire new ones. By looking at donation data with Fundraising Report Card®, we were able to pick up on the lapsed donors. Otherwise, our client may have focused only on overall growth and acquisition and missed lapsed donors entirely.

We were sharing screens and reviewing her Fundraising Report Card®.

I was hovering over her $5,000+ donor segment. When we exported the data we noticed an individual who upgraded from $250 in 2015 donations to $5,500 in contributions for 2016.

I asked a bit differently this time, “Do you think it cost you more than $5,750 to acquire this donor?”

Her answer, an emphatic, “No way!”

This story represents the reality that many development professionals face. From small organizations raising less than $250,000 annually, to large, multi-national NPOs whose assets top $100 million, there is a general lack of awareness when it comes to donor acquisition cost .

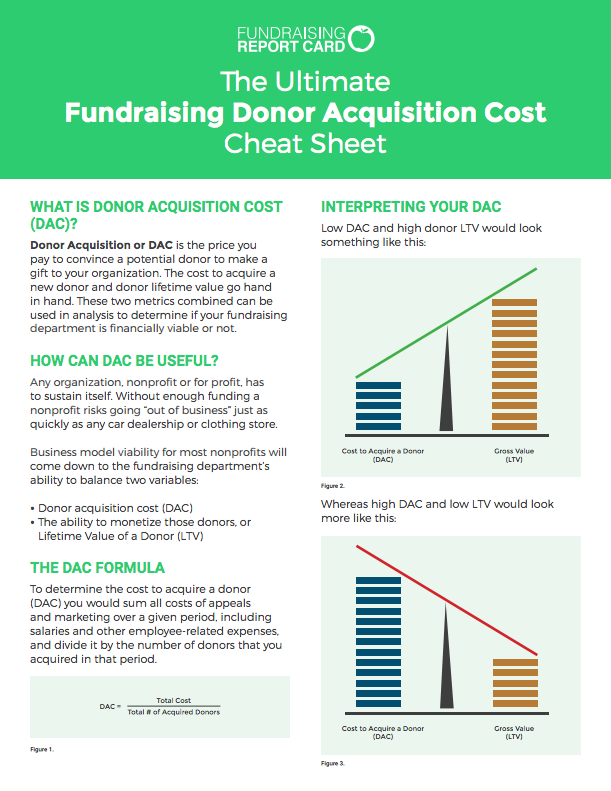

What is donor acquisition cost

We touched briefly on donor acquisition cost in part two of this series, Fundraising Metrics 101, but let’s review the definition once more.

Donor acquisition cost, or DAC, is the price you pay to convince a potential donor to make a gift to your organization . You can think of this as simply all the expenses that are attributable to acquiring a new donor. This can include expenses to third party vendors, postage, staff salaries, and other fundraising related costs.

Ultimately your donor acquisition cost formula will be:

You’ll interpret your DAC in a cost per donor context, i.e. “It cost us $25 to acquire each new donor from last month’s direct mail appeal.”

Note that in the example above we are also referencing DAC on a per appeal basis, “…from last month’s direct mail appeal.” Donor acquisition cost should almost always be broken down by fundraising campaign or activity. More on that a bit later.

How to calculate donor acquisition cost

Before we can get too deep into how you are going to leverage donor acquisition cost, we need to agree on how we are going to calculate it. Donor acquisition cost, unlike most other fundraising metrics, is loosely defined. “All expenses that are attributable to acquiring new donors.” That wording is vague to say the least. It begs the question, what are “all expenses?”

There are two general schools of thought here:

- Measure all fundraising expenses including staff salaries and overhead costs attributable to acquisition strategy

- Measure all fundraising expenses not including staff salaries and overhead costs attributable to acquisition strategy

Remember, you can download our Ultimate Fundraising Donor Acquisition Cost Cheat Sheet to have in your back pocket when sharing this with colleagues.

Which is better? And, still, what are “all expenses?”

From our research here at fundraisingreportcard.com (and this is mainly empirical and experience based), if you are a small nonprofit (less than 5 staff or small revenues), you are better off calculating your DAC without including salaries or overhead costs. If you are a large nonprofit (larger staff, larger revenues) you should calculate DAC both ways, with and without salaries and overhead costs.

Smaller shops generally don’t have the bandwidth to calculate DAC in both ways. If this is the case, save your time and focus on simply measuring “all fundraising expenses,” and leave out salaried costs in your DAC calculation.

Larger shops should have a greater capacity (there may be a full-time data analyst on staff) to measure and calculate DAC in both ways. If there are 15, 20, 25 development staff members, it becomes increasingly clear why taking into account their salaried cost is important. Human capital is a massive expense, and not factoring in that cost when calculating DAC would provide a distorted perspective. With that being said, calculating DAC in both ways, with and without salaries and overhead, is recommended to provide more clarity down the road. More on that in part four of this guide.

There are quite a few great resources that help outline what fundraising expenses really are. Take a peek at overheadmyth.com and nonprofitaccountingbasics.org for example!

The final question we still need to address is what are “all expenses?” When calculating donor acquisition cost you’ll want to consider any and all fundraising expenses attributable to a specific campaign. You’re not going to include the cost of the pen you use to take notes with, instead you’ll focus on the direct expenses related to fundraising. Here is a list common expenses you’ll want to include:

- Direct mail expenses (copywriting, design, mail handling, etc.)

- Campaign printing

- Postage

- Advertising

- Maintaining donor records (your donor management system)

- Conducting events

- Preparing materials (brochures, manuals, etc.)

- Email service provider expenses

- Software expenses

- Third party vendors

Why measure donor acquisition cost

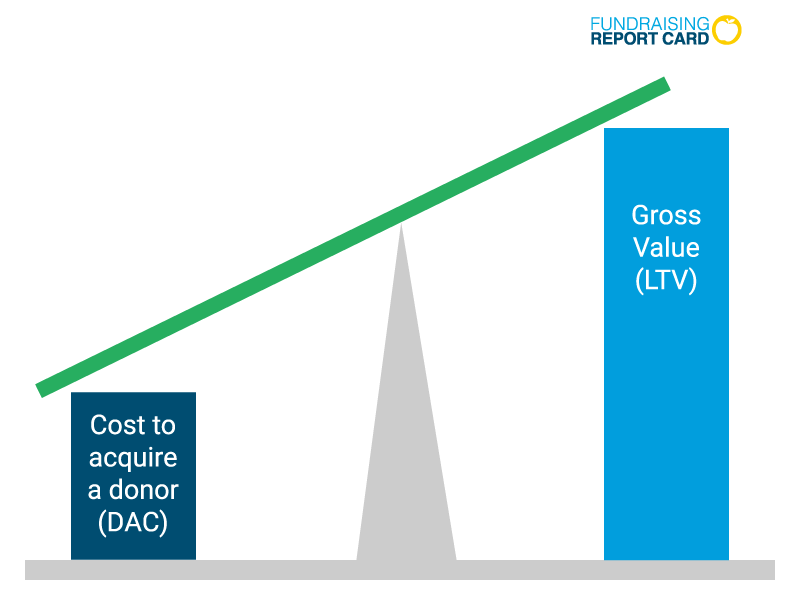

Donor acquisition cost takes on meaning when you pair it with other fundraising metrics. Donor lifetime value, for example, goes hand in hand with DAC to determine the “business viability” of your fundraising efforts. Yet as a stand alone metric, donor acquisition cost has lesser meaning. That’s not to say it is useless on its own (it isn’t), it simply means that DAC provides more meaningful insights when combined with other data.

DAC on its own does provide some insight. It can help leadership break through the “gut feel” decisions being made about budget allocation. For example, comparing donor acquisition costs by channel can shed light on where spending is out of hand and where there might be room for expansion.

Take for example a for-profit company like Gap Inc. Gap markets to their consumers in multiple ways, online advertisements, tv, radio, print, etc. Someone (or a whole department) at Gap keeps track of customer acquisition cost (CAC) broken down by acquisition channel.

The consumer (i.e you and me) doesn’t acknowledge which marketing channel we fall into when we buy clothes from Gap (did I click on a search ad or did I hear about a special on tv?). And we certainly don’t care what the Gap’s customer acquisition cost was (look, I just got these new pants!), but Gap is definitely keeping tabs on that. Because, at it’s core, CAC plays a vital role in determining the profitability of that marketing channel. If a channel is profitable, Gap will invest more in it. If it isn’t profitable, they’ll pivot and try something else.

Now, apply that concept to fundraising. Just as consumers want to buy pants, donors want to donate. Your organization most likely has multiple fundraising activities during the year. Direct mail, email campaigns, events, maybe even search ads. When a donor is acquired you’ll want to know not only which channel they came through, but also what the expense was to acquire them. That way, when you calculate your donor lifetime value (I promise we will do this in part four), you’ll be able to determine which fundraising activities are worth investing more in and which are worth pivoting away from.

Donor acquisition cost best practices

You’re going to want to capture and measure donor acquisition cost on a per campaign basis. As we touched on above, having this metric broken down by acquisition channel will empower us to find which fundraising activities are providing the best return on investment (ROI).

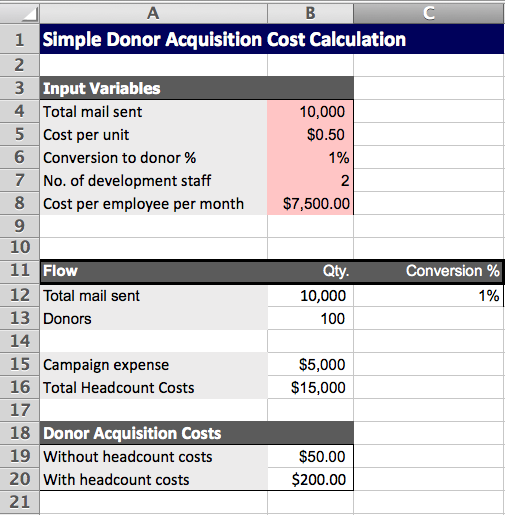

Yet, by this point you may be thinking, “This all sounds good and well, but how do I actually organize and calculate this stuff?” Our team thought of that as well, and that is why we are happy to share an Excel template that you can use today to start capturing, measuring and calculating your donor acquisition costs. You can download that right here. You’ll notice the template can be customized, but by default it is setup for measuring direct mail acquisition cost.

Most organizations keep track of DAC in an Excel spreadsheet like the one to the left, and although I have been known to bash Excel in the past, it actually does a really fine job of calculating and storing relatively simple data.

We aren’t going to be doing data visualization with donor acquisition cost, nor will we need to write some fancy equation to calculate it, and with that in mind, Excel becomes a great option for organizing and tracking DAC. Remember, you can download our template to get started measuring DAC today.

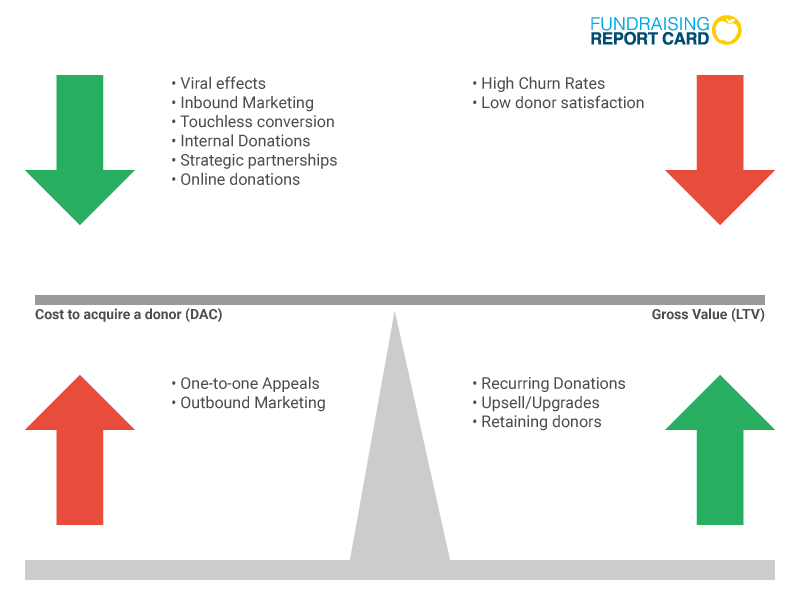

It’s also helpful to keep in mind what affects donor acquisition cost. Certain fundraising activities can actually decrease DAC, while others increase it. That may sound obvious on the surface, but a lot of organizations overlook DAC decreasing initiatives.

Take for example an investment in revamping your online donation page. The upfront, or sunk cost will be large. It is not cheap to redesign or create from scratch an online donation page. But, think about the decrease in donor acquisition cost. If the page is “touchless,” i.e no human being is involved to facilitate the donation, then the acquisition cost will be less than more high-touch efforts.

Key takeaways

- Donor acquisition cost, or DAC, is the price you pay to convince a potential donor to make a gift to your organization.

- There are two ways to calculate DAC: with or without salaried and overhead expenses.

- Donor acquisition cost paired with donor lifetime value can determine the “profitability” of your fundraising efforts.

Get Data-Driven Fundraiser Email Updates

NOTE: Thank you Jennifer Willett, Cheryl Papsch and Lizzie Weiland for editing this section of the guide.

Take me to part 2Take me to part 4