When you think of a successful nonprofit what do you think of? A good team? A passionate group of people? A large addressable “market?” Strong leadership?

Of all the characteristics of “success,” donor acquisition cost probably doesn’t come to mind.

Just like any for profit company, a successful and thriving nonprofit relies on a strong team, a good product (mission) and market fit (niche). Yet unfortunately, just like many for profit companies, nonprofits frequently “go out of business.” The culprit in many cases lies in customer, or in our case, donor acquisition cost.

Nonprofit fundraising business model

Any organization, nonprofit or for profit, has to sustain itself. Without enough funding a nonprofit risks going “out of business” just as quickly as any car dealership or clothing store.

Business model viability for most nonprofits will come down to the fundraising department’s ability to balance two variables:

- Donor acquisition cost (DAC)

- The ability to monetize those donors, or Lifetime Value of a Donor (LTV)

To determine the cost to acquire a donor (DAC) you would sum all costs of appeals and marketing over a given period, including salaries and other employee-related expenses, and divide it by the number of donors that you acquired in that period. (As donations are increasingly made online, it is also useful to look at donor acquisition cost without the employee-related overhead expenditures.)

To calculate LTV, you would estimate how much money you can expect to receive from a donor before they churn (leave). More on that equation can be found here.

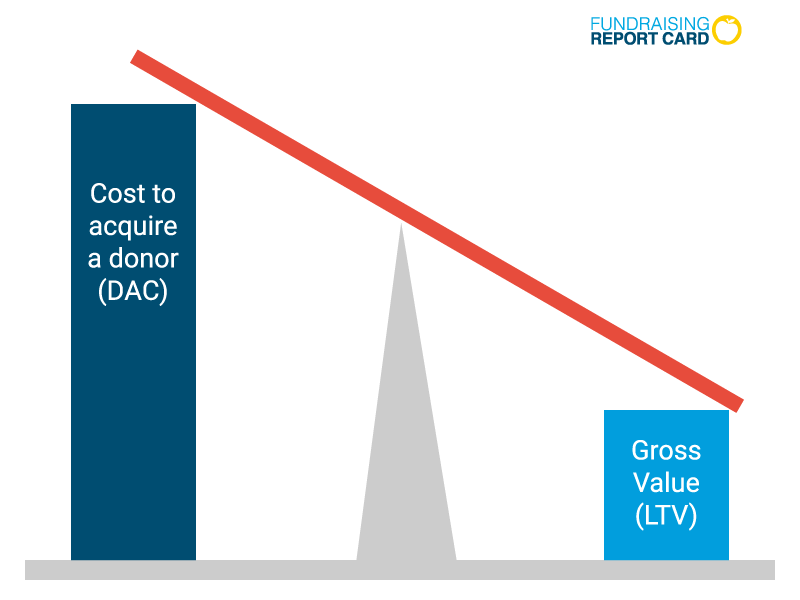

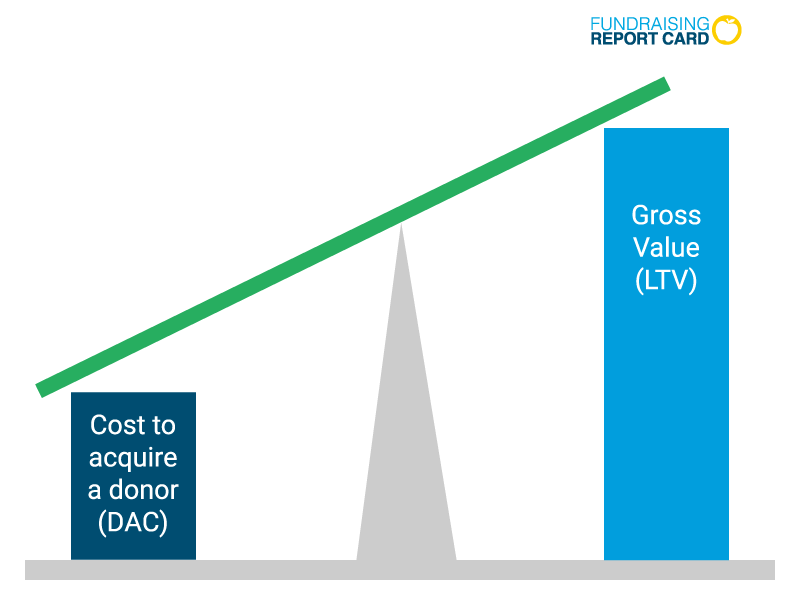

You don’t need a MBA from Wharton to see that business model failure comes when DAC exceeds LTV.

A well-performing fundraising department will have a significantly lower DAC than their LTV.

These two diagrams are so simple that you may be wondering why I included them in this article. But they perfectly illustrate the balancing act that is required to maintain a viable fundraising department. Of course, different factors affect the balance, but I’ll get into that with a more insightful diagram in just a minute.

Donor acquisition cost segmentation

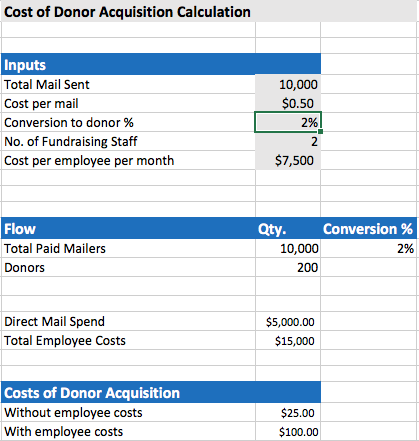

A good practice is to segment your DAC calculations. For example, if you are using direct mail to drive traffic to an online donation form you will want to track that cost with a spreadsheet similar to this:

Let’s imagine that the direct mailer in this example is a postcard, and it costs $.50 per piece. The organization expects to send 10,000 pieces and forecasts a 2% conversion rate. For our purposes we will consider a conversion to be when a new donor is acquired.

By segmenting costs, you can easily identify employee and vendor expenses attributed to DAC. The above example also works well for tracking annual fund or lower level donor acquisition campaigns.

You can imagine how high DAC can get when looking at only major, or principal donors. Employee-related expenses will rise, but so will the LTV of the newly acquired donor. To determine if your fundraising department is balanced in its expenses and donor value (gross revenue), it is crucial that you segment your DAC by giving level. Ideally, you want your LTV to far outweigh your DAC.

Balancing LTV with DAC

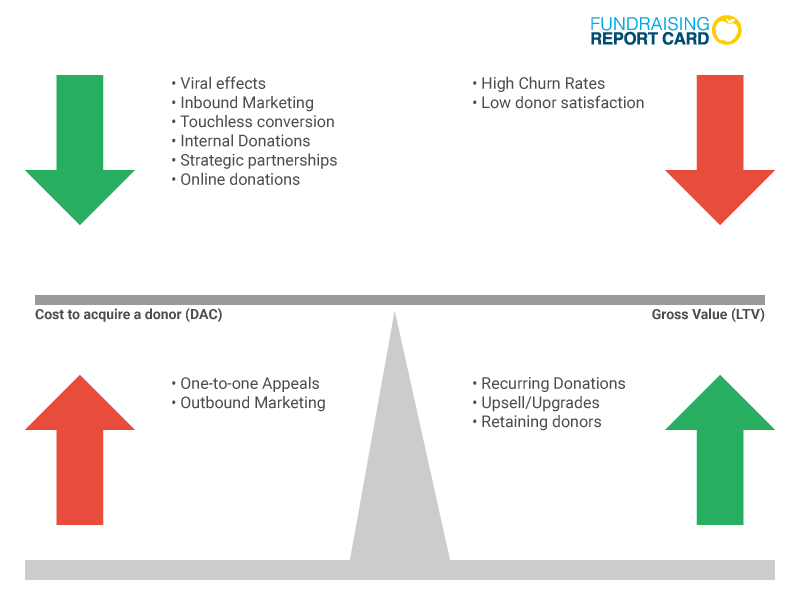

Take a look at the diagram below. There are several factors that can impact both LTV and DAC.

For example, the more your organization takes advantage of digital platforms, such as online donations, the more opportunity there is for your DAC to decrease. Likewise, it’s important to pay attention to overhead expenses that can increase LTV, such as visits with principle and major donors that help with donor satisfaction and retention. As you can see, it’s a very delicate balancing act.

Lessons learned — reduce DAC, increase LTV

In theory it’s simple: lower acquisition cost, increase lifetime value. Yet, in practice it will be more difficult. Sanitizing and organizing the data necessary to get to these metrics can be tricky. For DAC you’ll need to stay highly organized and utilize spreadsheets like the one above. For LTV we are trying our best here at the Fundraising Report Card® to help. We are working on segmented Donor Lifetime Value reports to help you focus on analysis and spend less time crunching numbers.

There are dozens of nonprofit marketing blogs and websites that preach ways to reduce DAC and increase LTV. In my experience it is best to test and measure, then rinse and repeat. Every organization (for profit or nonprofit) will experience different results when testing. But if you make sure to measure these tests, you’ll be able to recalibrate your department’s efforts and find what works best for your team. (Also, it doesn’t hurt to set a goal or two!)

Measuring these metrics may seem like an awful lot of work right now, but fear not! There’s a reason we’ve been working on the Fundraising Report Card® for over a year, and it is to help automate some of these calculations for you.

Making sure your fundraising business model stays in balance is undeniably important for achieving your organizational revenue goals, and fulfilling your mission. Our goal is to help make it that much easier to do!

Acknowledgments

I would like to thank my colleague at MarketSmart, Jennifer Willett for contributing greatly to this post.