Google search “fundraising metrics” and you’ll find plenty of blog posts and articles. In fact, you’ll come across too many. It can be overwhelming to figure out what fundraising metrics your nonprofit should track and measure. No two websites seem to offer the same suggestions, making it difficult to know what’s really worthwhile.

Fortunately, the Association of Fundraising Professionals (AFP) has come to the rescue (sort of).

Back in 2003 the AFP FEP (Fundraising Effectiveness Project) published a “Glossary of Terms” for its members and the public. (Some of us here at the Fundraising Report Card® even played a role in helping revise some of the definitions!) The document serves to ensure clarity and consistency across a variety of categories, terms, formulas, and most importantly fundraising metrics.

It’s is awesome because it establishes which fundraising metrics really matter. The downside is that it doesn’t specify which of the 68 fundraising metrics are most crucial to track.

Here at the Fundraising Report Card® we generate the majority of the AFP FEP metrics, but today, let’s focus on 3 simple fundraising metrics you can calculate on your own. It doesn’t matter if you’re wearing many hats at a small nonprofit or the executive director at a big organization, these are the 3 key metrics you should always have on hand.

Let’s get started!

Annual Overall Rate of Growth in Donations (%)

AFP FEP definition

Net of gains and losses in giving from last year (divided by) Total value of gifts received last year

Why measure it

It’s a safe bet to assume growing revenue (donations) is a high priority for your non-profit. When it comes to fundraising metrics, annual rate of growth will most obviously show whether your non-profit is succeeding in increasing donations or not.

Our friends at the AFP have laid out a straightforward definition. Net change (which could be a gain or loss), divided by the value of all donations received in the previous year.

This metric is most frequently associated with the annual Giving USA report. You may recall seeing headlines from this year that read, “Donations grow 4%…”

That is annual donation growth rate, and it is a crucial metric for all nonprofits to measure. Tracking changes in annual growth rate can inform strategic decisions and help you and your team set realistic fundraising goals each year.

How to calculate

To calculate annual donation growth rate you need two numbers: total donation revenue from this year (x), and the total donation revenue from last year (y). Simply subtract this year’s total from last, then divide that number by this year’s total and multiply by 100.

Analyzing several years of data will help you find trends and patterns in your database. And, it may be useful to segment the growth rate by giving level. This way you’ll have a more complete view of your organization’s fundraising efforts at each level.

Visualize it

After calculating your donation growth rate, you should graph it. Computers are great at reading lines of data in a spreadsheet, but for most of us humans, visual representations are much easier to interpret.

In the past graphing required extensive Excel knowledge and usually meant a whole day spent working with pivot tables and spreadsheets. Oh, how times have changed!

One of the great things about the free Fundraising Report Card® Core is that it comes with built-in donation and donor growth rate charting. Simply upload your data file and you’ll see your annual growth rate in a Column Chart.

Annual Average Gift ($)

AFP FEP definition

Total dollars received (divided by) Total number of gifts received (times) 100

Why measure it

Spotting trends in average gift size can speak volumes to the state of your organization’s fundraising health. Think of a for-profit business — let’s say an ice cream shop. Instead of calculating average gift per donor this business would calculate average transaction amount per costumer.

The shop may sell items other than plain ice-cream. They might offer sandwiches or coffee. Why? To increase the average transaction amount per costumer. Larger transactions generally equate to larger profits.

The same principle applies at a nonprofit. Nonprofits can employ similar tactics to boost their average contribution amount. Maybe it’s something as simple as adding an extra checkbox to an online donation form, “Would you like to increase your gift by 5% to help with overhead expenses?”

Measuring annual average gift amount will help you understand who your donors are and how they give. Plus, you can easily measure average gift size on a per campaign or per donor segment basis.

How to calculate

To calculate average gift amount you only need two numbers: Total donation revenue and total gifts received. Just divide donation revenue (x) by the number of gifts (y) and you have average gift size. Simple, right?

You can take it a step further and calculate the change in annual average gift amount. Simply take this year’s average gift amount (a), subtract it from last year’s amount (b), divide by this year’s amount and multiply by 100.

Visualize it

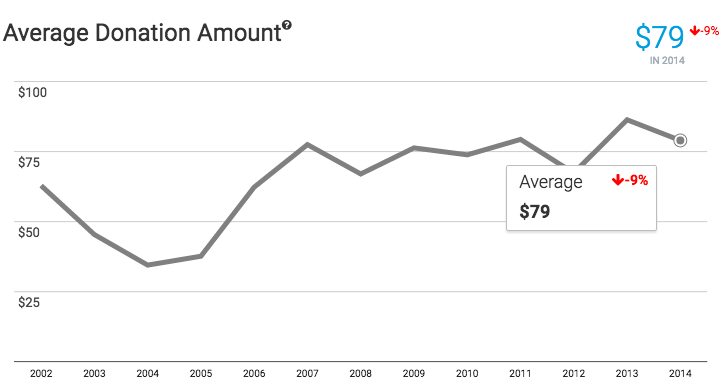

Spotting trends in average gift size is pretty easy in a spreadsheet, but it never hurts to look at it graphically as well. When plotting average gift amount, you’ll want to use a line chart — and hopefully, the line is moving up and to the right.

Plateauing or decreasing average gift amounts become visually apparent when viewing them in a graph. For example, in this graph you can easily see the organization increased average gift amount in the long run, but has recently experienced some stagnation and decline.

Donor Lifetime Value ($)

AFP FEP definition

Average annual giving by a donor (times) Estimated donor lifetime (years)

Why measure it

Another crucial metric all fundraising teams should calculate is donor lifetime value. This metric has it’s roots in the for-profit sector and for good reason. Companies use this metric to calculate customer acquisition cost, but nonprofits can apply the same logic to fundraising.Donor lifetime value is a more comprehensive metric than average gift amount. Gift amount only takes into account the size of a donation, whereas lifetime value considers how long a donor stays with your organization as well.

Lifetime value (or LTV) is a prediction of how much money you can expect to receive from a donor before they churn. This metric can help you and your team make important decisions about how much to spend to acquire and retain donors.

How to calculate

Calculating LTV is simple, but it relies on a few other metrics that can be tricky to calculate. You’ll need donor lifespan, average donation amount, and frequency of donation.

The formula looks something like: LTV = Lifespan × Average donation amount × (Total # of donations ÷ Total # of donors)

Pulling this information from your database might be difficult, but it’s worth the hassle. Once you know your LTV, you can set your donor acquisition cost and be more savvy with your marketing expenses.

Visualize it

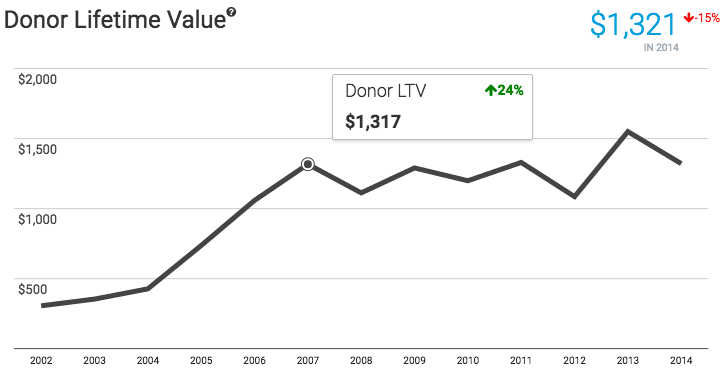

Graphing donor LTV is unbelievably important. Looking at year-to-year changes in lifetime value can greatly alter your fundraising strategy.

Just like with average gift, visualize LTV with a line chart. It becomes overwhelmingly clear which direction your organization is going when you plot your lifetime value numbers.

These 3 metrics are barely scratching the surface when it comes to fundraising analytics, but they are a good place to start.

If you want to see how your organization’s metrics measure up, you can drag and drop your data today into the Fundraising Report Card®. You’ll instantly get insights into your Growth Rate, LTV and more in just a few clicks. Or, If you’re interested in learning how to calculate more metrics on your own take a look at our Help Center for formulas and tips.

This is the problem when quants take on issues they don’t understand. What happens when a big gift comes in — perhaps one that you spent several years cultivating. Based on these formulas, it will make your program look like it is declining in the following years.

These these kinds of metrics are very useful for programs with large donor bases contributing small numbers of gifts. But, guess what? That’s never been the most efficient model for raising money.

Unfortunately, this kind of blind application of poorly-constructed evaluation tools — or should I say, lazily-constructed evaluation tools — is having a negative impact on development programs. Now, these folks have to worry about the ratings they are getting from online programs like this that don’t really know what they are talking about. Thanks, guys.

Hi Michael, thank you for the comment!

I think what you’ve said has a lot of merit.

What is great here is the fact that we considered the exact circumstances you outlined when developing the Fundraising Report Card. We worked with dozens of folks in the industry ranging from experts at the Fundraising Effectiveness Project to veteran fundraising consultants to glean the knowledge that us “quants” lack.

If you have a chance, I would recommend creating a free account to the Fundraising Report Card. I think you’ll see pretty quickly that we do no “ratings”, and instead focus on helping you simplify your complex donor data.

P.S. I reached out to you via email — if you have the time I would love to chat more about this over the phone.

One way in which one might address the issue that Michael raised is to pull out the large, one-off gifts such as a realized bequest or income from a one-time event (think Ice-Bucket Challenge if you are the ALS Foundation) then do the calculations.

One might also need to consider other events that could impact giving. For example, there might be a high profile legal case in the news that relates to the mission of the NPO, e.g., child abuse. If the NPO takes steps to capitalize on that news and bring in more donors they might see a great bump in numbers of donors and gifts, but unless steps are taken to try and retain those donors numbers might regress to the mean. Such events need to be noted when numbers are reported (and I believe numbers should always be accompanied by narrative that offers insight about what they mean and do not mean).

“Numbers should always be accompanied by narrative that offers insight about what they mean and do not mean” — I couldn’t agree more. Thank you for your comment, very insightful!

Sophie,

From a statistical viewpoint, you are entirely correct. Removing outliers will give you a better analysis of the “non-outliers.” And this is just fine if you are running a mass solicitation program (i.e. direct mail, phonathons) — but not even with these.

The problem here is that serious fundraising is, to a very significant degree, a “Black Swan” enterprise. It is precisely those outliers that have the biggest impact on a charity. These statistical models — of which this report card is but one example — do not encourage pursuit of such gifts, which often take time to solicit and bring in. Worse yet, they make the charity look bad in years after they are booked.

The other issue they ignore is that different development programs have different financial ratios, and that the programs used by charities are often dictated by circumstance. For example, an organization for whom agressive direct mail acquisition programs make sense will have terrible report cards which will harm them with donors, even though they are pursuing a correct strategy.

I guess the simplest way to express this would be to ask you to consider an analogy.

Imagine a financial analyst was running around claiming that they had identified a set of one-size-fits all metrics for evaluating the effectiveness of any for-profit business. No one in the financial services industry would take such a metric seriously, because they know very well that different industries operate on often very different financial ratios.

I don’t see why such an approach makes any more sense in the very diverse world of philanthropy, either.

Net of gains and losses in giving from last year (divided by) Total value of gifts received last year:

(x-y)/y not (x-y)/x

Thank you!

Interesting chat Michael/Zach, my take on this is that there is a real lack of financial analysis and understanding at senior fundraising manager level. Whilst you can argue about the shortcomings some of these tools may have in various scenarios, it is still the fundraiser’s responsibility to produce the analysis combined with the narrative that contextualizes the data and assesses how that reflects the business plan. This is all the more important at a time when trustees are being reminded of their accountability and will therefore need to achieve a greater understanding of the efficacy of fundraising programmes. The danger to my mind of the ‘black swan’ tag is that the implication is that fundraising is more akin to an art and should not be subject to conventional analysis and the fundraising managers should be left to their own devices.

Julian, thank you for providing your perspective. I found myself nodding my head in agreement as read your comment. Thanks for sharing.

No, Julian. What I mean when I refer to as a “black swan” events is the fact that fundraising is field where the Pareto Principle (80 percent of output come from 20 percent of donors) is — or should be — the norm. Consider, I have one client who, over the past three years or so, I have helped secure individuals gifts of $800,000 and $500,000 and $1 million. Their normal annual fundraising gross revenues run about $250,000. This is not unusual. Commonly, one third or more of a typical fundraising campaign’s revenues come from ten or fewer gifts.

Moreover, the linear nature of fundraising results lend themselves to plenty of financial analysis. There is no shortage of it in my 34 years of experience in the field.

That said, one area where I find great weakness is in the area of special events accounting. The common error is to include only direct costs when calculating a bottom line. Indirect costs — most commonly the many hours of salaried staff time — don’t get factored in, even though many of these events consume large quantities of such time.

Wanted to ask for a bit more detail on calculating donor lifespan. Is this how long you expect a donor to live (based on actuarial numbers)? Or does it mean looking at your database to see how long, historically, donors have stayed with your organisation after a first gift, and using that as the figure in your ‘lifespan’ formula? I guess part of the aim of measuring the metric is to make the second one longer

Thank you, helpful article!

Hi Simon,

Thanks for the comment. In this context lifespan refers to how long (in time) you can expect to receive donations from a donor before they churn. The equation ends up looking something like this: Lifespan = cumulative years of giving ÷ total # of donors

You are right though, you’ll want lifespan to increase over time! Hopefully more donors are being retained which will help increase the lifespan metric.

I took a peak at your website, morepartnership.com, it looks like you all do some interesting work. Thanks for checking out our blog!

I agree with Michael that lifetime metrics work for annual giving programs but don’t fit well with major giving programs. I’m wondering if there would be some way of “amortizing” large gifts – in the case of pledges, perhaps counting payments rather than revenue, or using some other formula? I’m no metrics guru, so I don’t know if this would be either advisable or feasible.

For the first metric, why is “this year” = x, then suddenly for the formula, “this year” = y on the bottom??

Does anyone have a dashboard of metrics – even a template – that you might share?